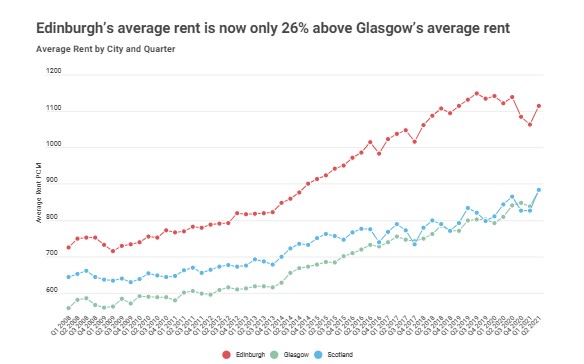

Average Rent

In terms of average rent, Edinburgh is more expensive than Glasgow, with the average rent in Q2 2021 in the Capital reaching £1,115pcm compared to £882pcm in Glasgow. However, what is notable is that, while this represents a premium of 26% for the average Edinburgh rent compared to the average Glasgow rent, this gap has narrowed sharply over the past 2 years.

Over 2018 and 2019, the average rental difference between the two cities peaked at 44%, above the long-term average of around 35%. This sharp narrowing of premium between average rent has been a function of the unique circumstances impacting the Edinburgh market, particularly around the rise and fall of the short-term lets sector, while Glasgow has remained more consistent.

A comparison of average rents on a £/sqft basis shows the difference between the two cities. The average £/sqft rate in Edinburgh’s City Centre is around the £19/sqft rate, weakening to low double digits in more outlying areas. In Glasgow, the desirable West End averages around £14/sqft. This represents a premium of over a quarter on the city on a £/sqft basis, where average £/sqft rents are in single digits in most areas.

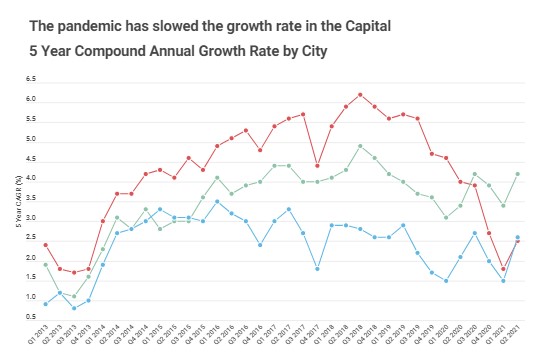

Growth Rates

The change in market dynamics between the two cities is perhaps best illustrated by growth rates over time. The strong growth experienced in Edinburgh from 2014 onwards can be seen below. The compound annual growth rate (CAGR), based on the preceding 5 years, peaked at over 6% in 2018 having been above 4% for the previous 4 years. In Glasgow, the 5-year CAGR peaked at 4.9%. A number of factors came together to drive down Edinburgh rents.

First, the Edinburgh market had seen a period of exceptionally strong growth to 2019, so had already entered a period of slowing growth before the pandemic. When the Covid-19 pandemic arrived and restricted flat moves, economic migration, tourism and student demand, the market in Edinburgh cooled more dramatically, with average rents falling in the city by over 1% year on year. Despite the pandemic, Glasgow average rents rose 9% from £810pcm to £882pcm. This has meant that, in the five years to Q2 2021, the compound annual growth rate in Edinburgh has fallen to 2.5% while Glasgow has remained consistently above 4.5%.

First, the Edinburgh market had seen a period of exceptionally strong growth to 2019, so had already entered a period of slowing growth before the pandemic. When the Covid-19 pandemic arrived and restricted flat moves, economic migration, tourism and student demand, the market in Edinburgh cooled more dramatically, with average rents falling in the city by over 1% year on year. Despite the pandemic, Glasgow average rents rose 9% from £810pcm to £882pcm. This has meant that, in the five years to Q2 2021, the compound annual growth rate in Edinburgh has fallen to 2.5% while Glasgow has remained consistently above 4.5%.

Outlook

So where does this leave the rivalry? Edinburgh’s rental market has clearly been more impacted by the pandemic, with key sectors of the economy, which drive rental demand, being accutely impacted. By contrast, Glasgow’s rental sector has remained more stable resulting in strong growth figures over the short- to medium-term. With lockdown restrictions easing, tourism returning and economic migration resuming, average rents in Edinburgh have already returned to postive growth in Q2 2021. For Glasgow, economic recovery is also expected to drive demand and support consistent rental values in the city moving forward.

While much has been made of the flight from cities and the rise of remote working, while different in character, both cities are similar in offering vibrant and economically dynamic urban lifestyles and quality of living. It is for these similarities, rather than their differences, that we expect urban demand for both rental investment and rental living to return over the latter half of 2021 and into the future.