Key findings explored.

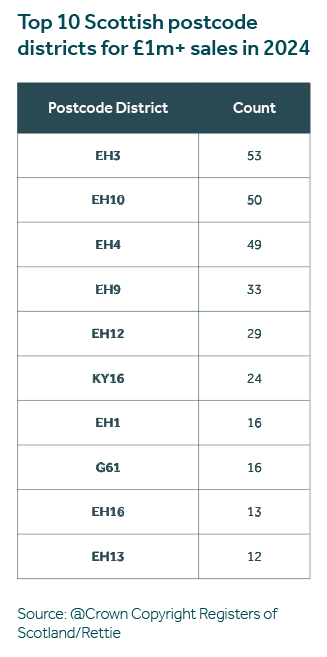

1. EH3 is the top performing area for £1 million sales in the country.

EH3, which covers Edinburgh’s New Town and West End, has taken the top spot with 53 £1m+ sales in 2024 - up 7 year-on-year. This growth reflects sustained demand for centrally located, architecturally significant homes within walking distance of key city amenities, excellent schools, and cultural institutions. With limited stock and international appeal, EH3 has firmly reasserted itself as Edinburgh’s most sought-after postcode for prime buyers.

EH4 - encompassing Barnton, Cramond and Cammo - also saw a significant rise, with £1m+ sales increasing by nearly 50% in 2024 to 49. This jump underscores a growing preference for high-quality suburban living within reach of the city, particularly among upsizing families.

Other key Edinburgh postcodes - EH10, EH9, and EH12 - round up the top five, together accounting for over 40% of Scotland’s £1m+ sales,

illustrating the enduring dominance of the capital’s prime core.

Postcodes outside Edinburgh that made the top 10 include KY16 (St Andrews) and G61 (Bearsden) - the latter being the only West of Scotland area to feature in the Top 10, highlighting the continued concentration of high-value activity in the East.

2. The growth in high value sales is driven by the East.

In 2024, Edinburgh alone accounted for 56% of all £1m+ transactions in Scotland - up six percentage points from 2023. This rise speaks to the city’s broad-based appeal, combining economic stability, historic character, and a strong schooling offering, which continues to attract both domestic and international buyers.

Beyond Edinburgh, the East remains the most dynamic region. St Andrews (KY16) recorded 24 £1m+ sales in 2024, supported by a steady stream of interest from returning alumni, second-home buyers, and retirees. Coastal towns like North Berwick (EH39) and Elie (KY9) also performed well, benefiting from lifestyle-driven relocation trends and an enduring post-pandemic shift toward more spacious, scenic living environments.

Conversely, Glasgow and the West has seen its share of the £1m+ market contract, falling from 26% in 2023 to 17% in 2024, with the notable exception of Bearsden (G61), where sales rose to 16. While Glasgow continues to face some headwinds, there are signs in 2025 of renewed interest as affordability in the capital tightens.

Interestingly, early 2025 data (Q1) suggests a modest rebalancing: Edinburgh and the East’s market share has dipped to 66%, while Glasgow and the West has begun to regain ground, rising to 28%.

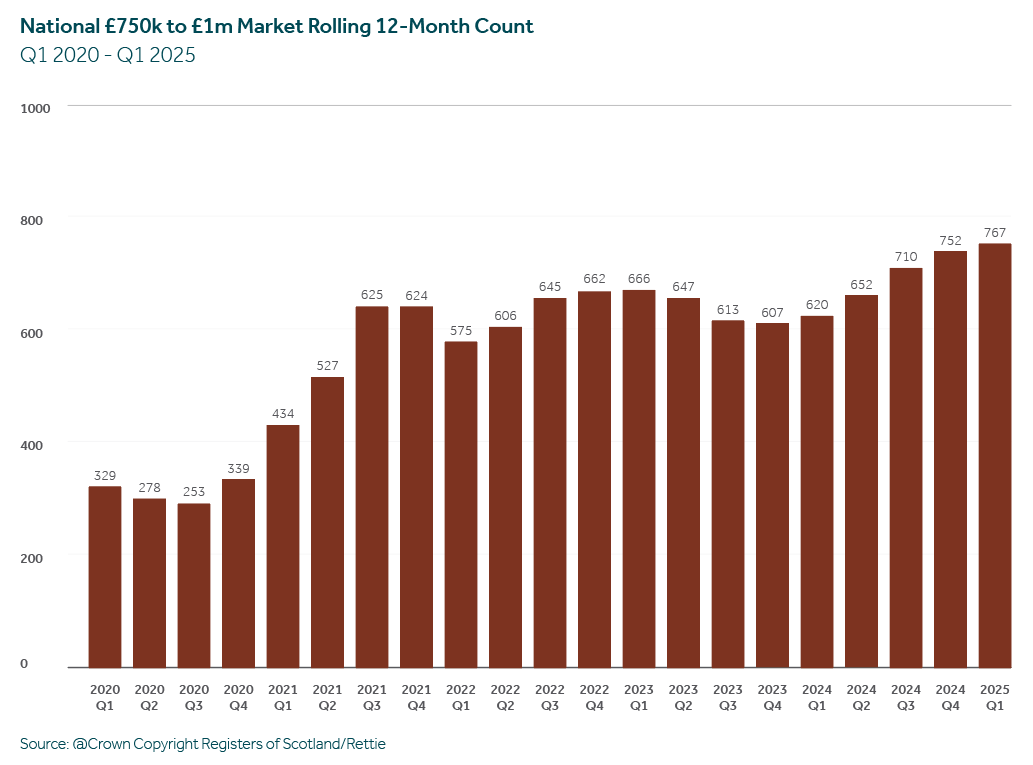

3. There has been strong growth in the £750k-£1m market.

While the £1m+ segment has remained broadly stable since 2022, the market directly below it has surged. On a rolling 12-month basis, sales between £750k and £1m reached 767 at Q1 2025 - an increase of nearly 25% year-on-year.

This uptick reflects improved affordability as mortgage rates stabilise and buyer sentiment recovers. It’s also an indicator of future growth at the top end: as values appreciate and more homes move into the £1m+ bracket, this middle-prime tier is likely to fuel future expansion in Scotland’s high-value market.