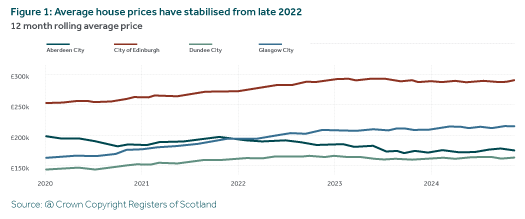

Sales market maintains stability.

On a 12-month rolling basis, Glasgow led the way among Scotland’s main cities in 2024, with the average house price increasing by 2.3%. The rise in Edinburgh average prices was just 0.6% and the other main cities also experienced flat price changes. This continues a trend identifiable from late 2022.

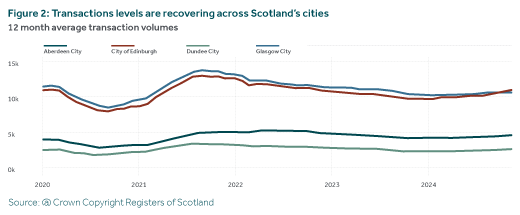

The number of house sales in 2024 rose across the country by 5% and there was a modest uptick in most parts of Scotland. This was a welcome change to the previous two years, which saw cumulative declines exceeding 10%.

The rebound was mainly driven by lower mortgage rates and better access to credit, especially for the likes of first-time buyers, which has helped to get transaction chains moving again. However, this improvement in market conditions has been modest as lending remains more expensive and restricted than prior to late 2022.

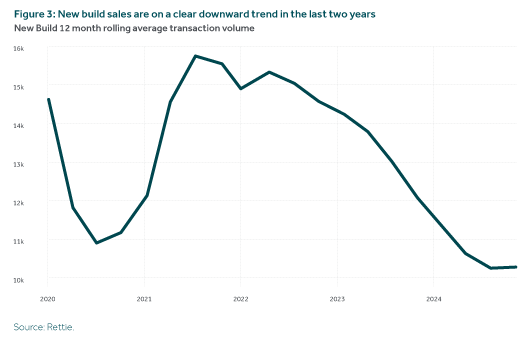

New build remains in retreat.

The new build market continued to struggle throughout 2024, as the industry has been affected by demand-side and supply-side impacts from the cost-of-living crisis and higher interest rate environment, combined with a more difficult and costly regulatory environment.

Overall, new build sales were down 14% in Scotland in 2024, although did show signs of stabilising, with pockets of activity, at year end.

New build sales only accounted for 11% of all Scottish house sales in 2024, a figure that is normally around 15% in recent years.

The average price of a new build in Scotland has continued to rise and is now around £329,000 (up 2.2% YOY), but incentives are commonly being used at approximately 3-5% of gross sales prices, meaning that, in net terms, prices are likely falling in most locations.

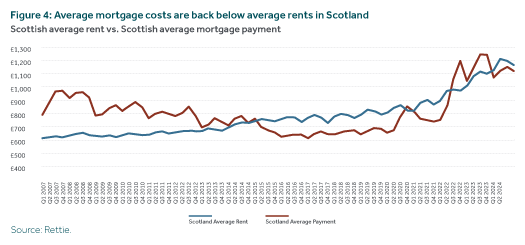

Mortgage affordability improves.

The greater relative affordability of house buying, particularly in relation to renting, improved in the 2010s, with the cost of the average mortgage payment (based on average 2-year fixed rate mortgage at 85% loan to value) below that of the average rent over much of the 2015-22 period.

Sharply rising mortgage costs from Autum 2022 reversed this position, providing greater incentives, especially for the likes of potential first-time buyers, to rent rather than buy. As inflation has cooled and mortgage rates have fallen, the affordability of house buying has improved. The average mortgage payment in Scotland was at £1,125pcm in late 2024, a little lower than the average rent in Scotland.

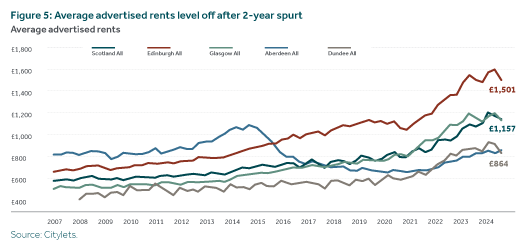

Rental market has cooled but availability remains reduced.

Average advertised rents (new rents between tenancies) in the private rented sector (PRS) cooled in 2024 after substantial rises throughout 2022-23. This is evident across the main cities as well as Scotland as a whole.

The Scottish Government’s rent freeze and then cap within tenancies had the effect of pushing up rent rises between tenancies. There was also the incentive for landlords who had been under-renting properties to push these to market value as soon as they could, given the later rent adjudication process was based on this. This now seems to have worked its way through the system, but, overall, probably means that Scotland has higher rents

than it would have had without the policy intervention.

Our Market Outlook and Forecasts.

While mortgage rates are now reducing, they will remain above historic levels for a time, maintaining a headwind for the market. This is likely to exert continued downward pressure on house prices across Scotland. There remains active demand, although considerably weaker than in 2021 to mid-2022.

The latest Bank of England Monetary Policy Committee report expects the overall economy to be stagnant in 2025, with modest growth in the succeeding two years. Inflation is also expected to be close to 3% (and above target) over 2025 and 2026, meaning that the scope for further reductions in interest rates (after the 0.25 percentage points cut in early 2025) will be limited. The markets are expecting another two 0.25 percentage point cuts in 2025, which will help boost economic and housing market activity (but only to a slight extent) and there will be borrowers approaching the end of their current generous mortgage terms who will need to be refinancing at higher rates than they did a few years ago.

Our market forecasts have been reasonably good in recent years. Looking at the outturn from our similar briefing last year, we correctly forecast limited price growth and transaction recovery in 2024.

For 2025, in our central forecast, we expect average prices to rise this year by around 3%. With stronger economic performance from 2026, we expect to be moving back closer to the long-term trend (of around 4%) in subsequent years. It will take time for the whole market to adjust to higher interest rates, as people gradually come off fixed term deals, which will probably lead to average house price growth at modest levels for a time.

Sales activity recovered slowly in 2024 and close again to its 10-year average. Another year of gradual improvement in 2025 should move us back to this longer-term trend of c.100,000 sales per year, still some way below the 154,000 sales in 2007 at the market peak.

This will vary across geographies and property types.

In terms of the rental market, the cost of the average mortgage falling below the average advertised rent may ease some of the pressures on the private rented sector (PRS) as demand dampens a little. This is already being seen in the main cities, although sharper reductions in supply may increase pressures again because of legislative change.