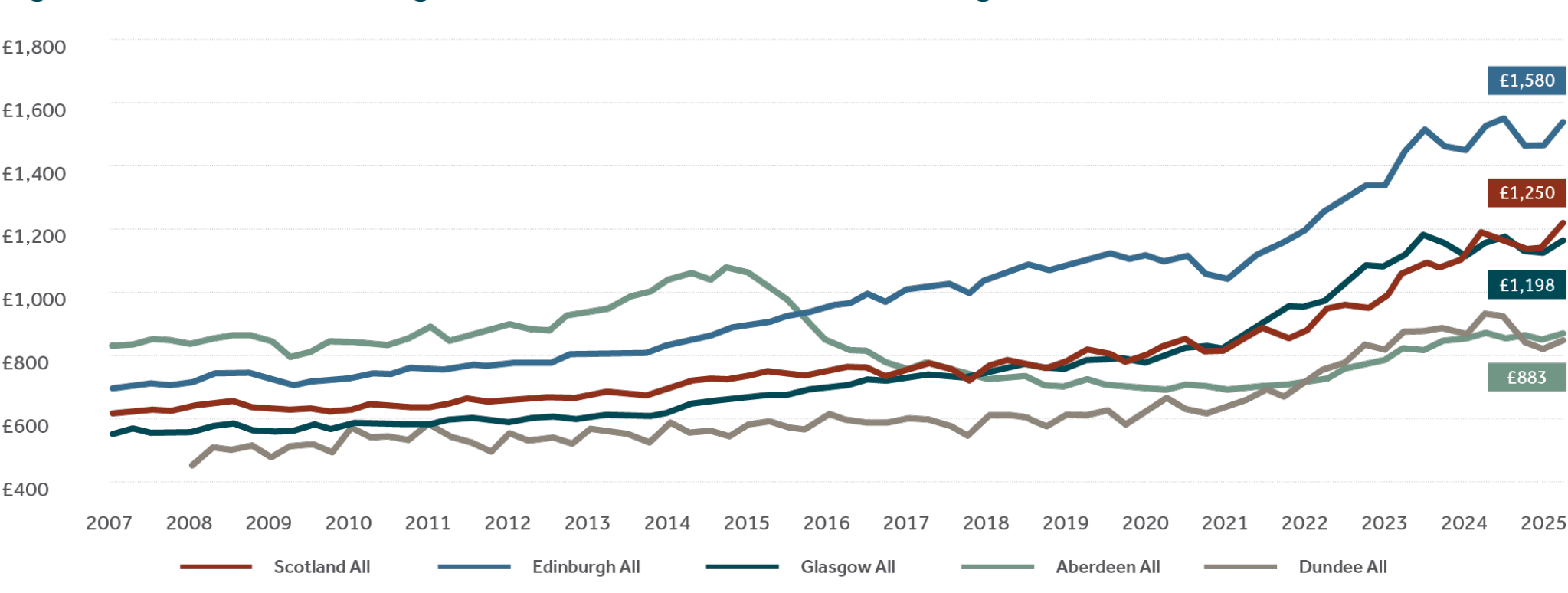

Glasgow leads Scottish cities in house price growth.

On a 12-month rolling basis, the average house price in Glasgow has continued to outpace Scotland’s main cities, growing by over 5% to nearly £218,000. Edinburgh and Dundee have both grown by c.1%, while the average price in Aberdeen has continued to decline (down 1.2%). However, the average house price in Edinburgh (c.£338,000) continues to surpass other areas.

In 2025, (Jan-Aug) the number of house sales has risen by 5.5% YOY as the market continues to recover from the slump over 2022-23.

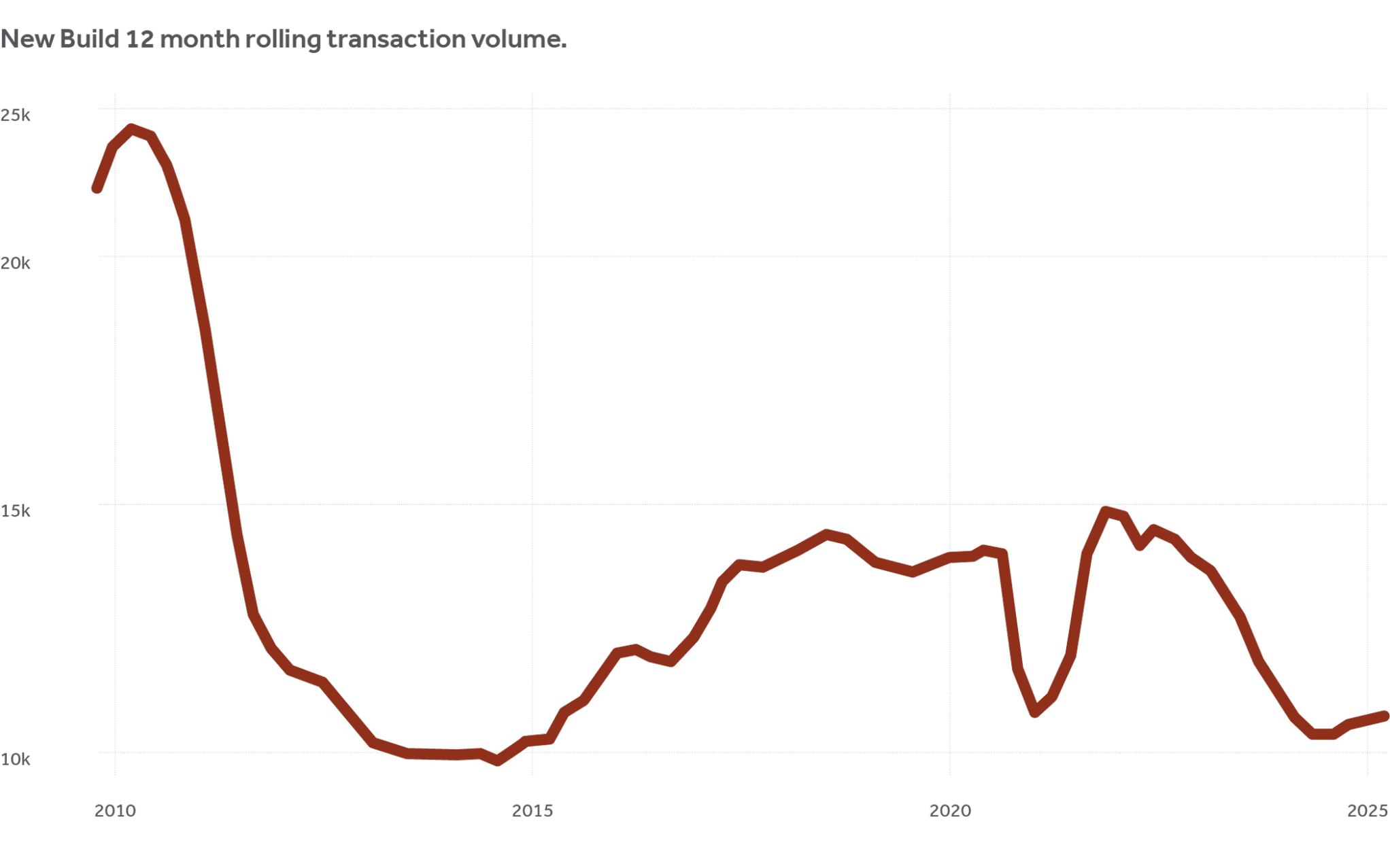

New build market begins recovery.

The rebound in overall market activity is finally extending into the new build market, which has had a similar increase in sales as the second-hand market in 2025 to date. Despite the increase through the first half of 2025, new build sales continue to make-up a smaller proportion of Scotland’s total sales. In 2025, new build sales only account for 10% of all Scottish house sales, down from the historical average of 15%.

Rental market reaches all time high.

The average advertised rent in Scotland rose sharply following the Covid-19 pandemic and currently stands at £1,250pcm as of Q2 2025, which is the highest on record. Over the last three years, the average rent has grown at a compounded annual rate of 9.4% nationally, which is more than double the ten-year rate. The recent growth reflects the diminishing rental supply and persistent demand, particularly among students and young adults. However, it has also been caused by political intervention.

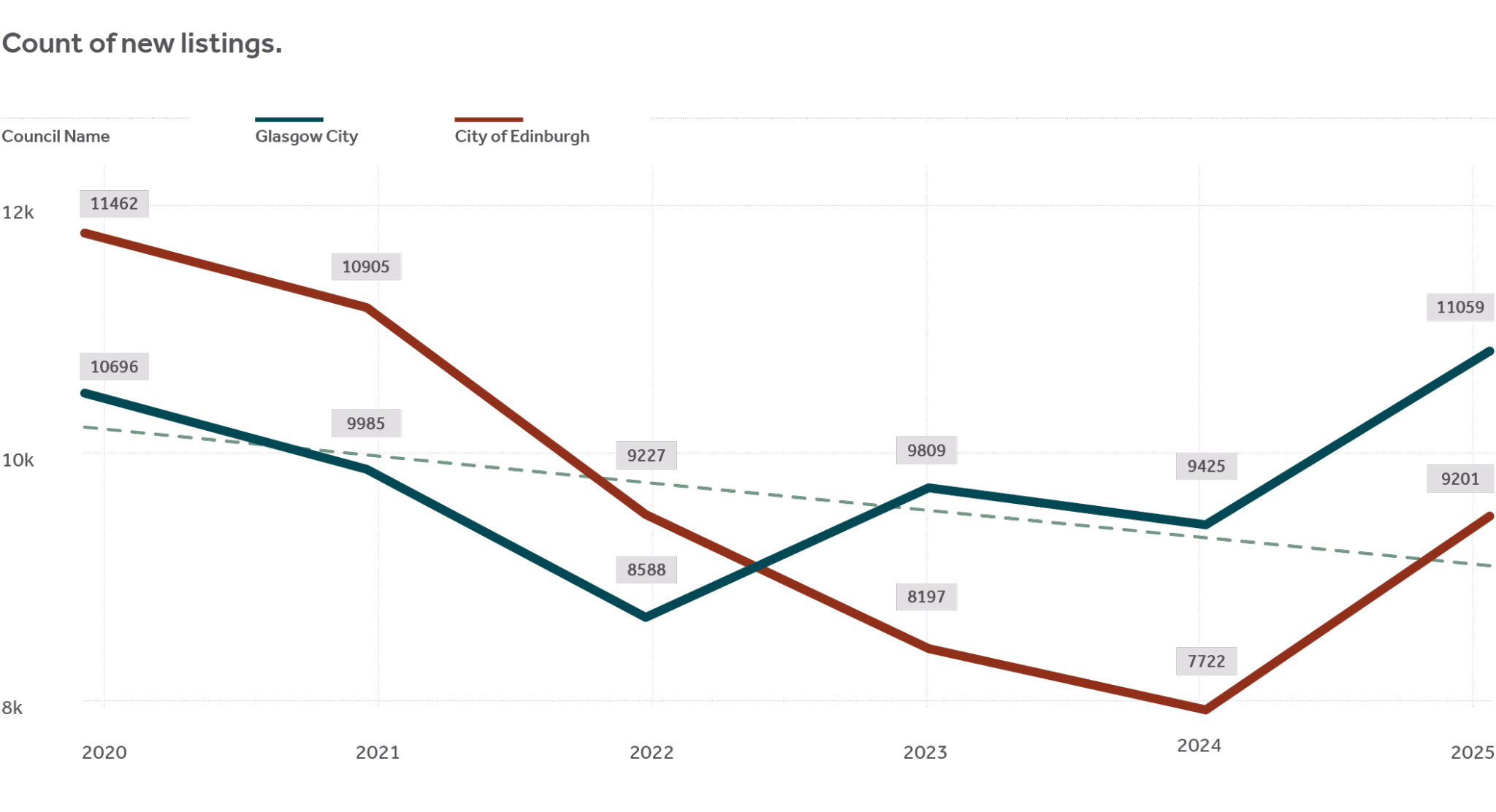

In the first half of 2025, the number of listings has increased modestly on a YOY basis (up 3%), indicating that rental availability may have bottomed out.

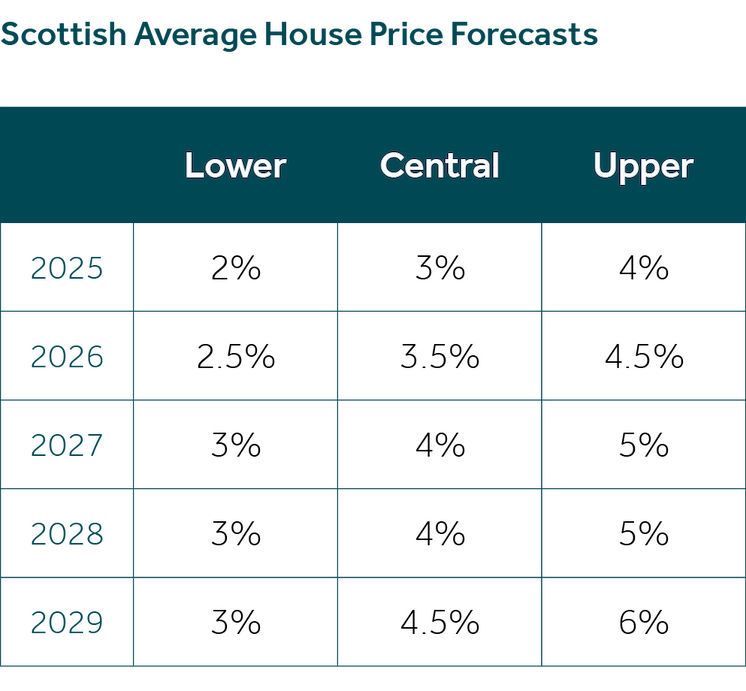

Market Outlook & Forecasts.

Falling mortgage rates and rising rents are continuing to nudge the sales market in a positive direction. The implementation of the UK Government’s mortgage guarantee scheme should provide further tailwinds to market activity through helping first-time buyers expand their access to credit.

Recent economic forecasts from the Bank of England Monetary Policy Committee report suggests modest GDP growth over the next three years. Market expectations are that interest rates will remain around 3.5-4% for the foreseeable future.

Our market forecasts throughout the first half of 2025 are on track for a rise in average prices of 3% by the end of the year. We expect similar growth in the following years, supported by modest disinflation and moderate increases in economic growth.

Sales activity has quickened slightly above expectations, in part due to government initiatives and falling mortgage rates. We forecasted a 2% rise in sales activity, equating to 100,000 sales for the calendar year. In 2025 (Jan-Aug), sales activity suggests a rise of 5% over the year to c.103,000 by the end of 2025. This will vary across geographies and property types.

In terms of the rental market, further rental growth may be limited due to a notable return of rental stock back onto the market. In addition, more renters may be able to access sufficient financing due to the mortgage guaranteed scheme to place a deposit on a house, where the average monthly payment is now 15% below the average rental payment. However, this will be counterbalanced to some extent by landlords moving rents to market values over the next two years in circumstances where they are currently ‘under renting’.