Key findings explored.

1. 7 in 10 house sales now pay LBTT

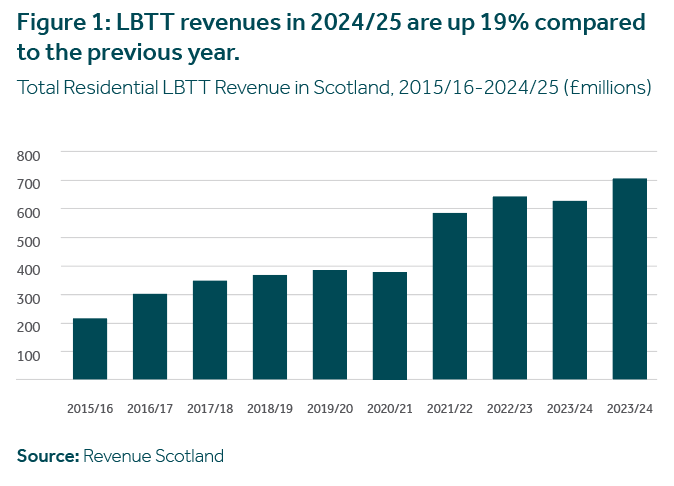

Residential LBTT revenues increased over 2024/25, up by c.19% on 2023/24 levels, which had been relatively weak compared with previous years.

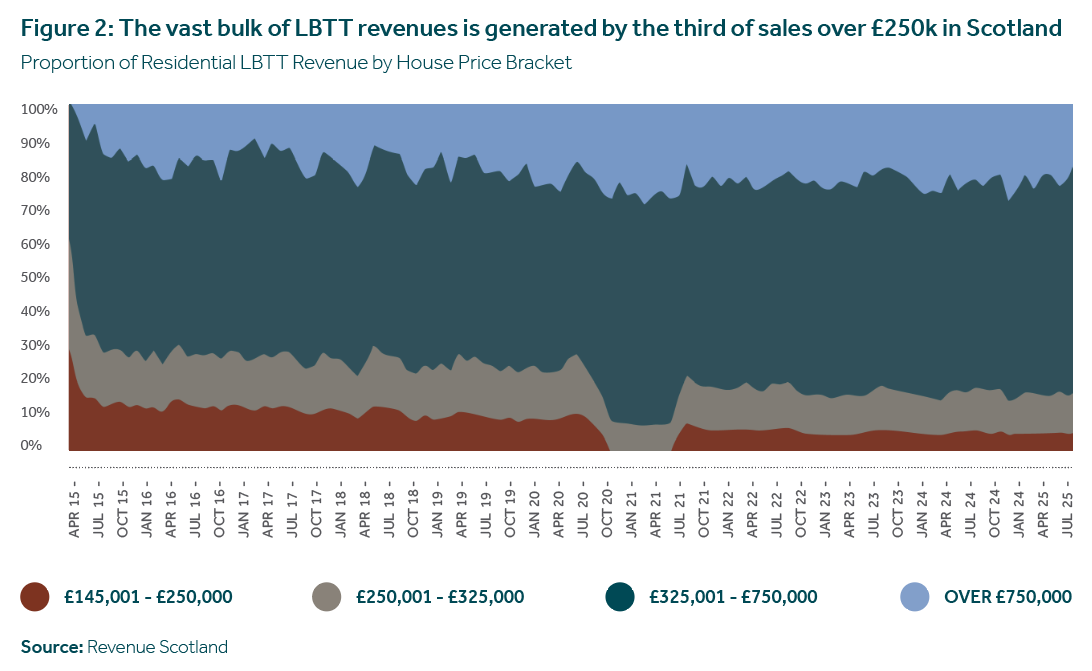

When LBTT was introduced in 2015/16, over 50% of transactions met the £145,000 threshold. However, as house prices have risen (and bands have not been adjusted), around 70% of sales are in the LBTT orbit.

Similar to the previous year, in 2024/25, a third of sales were above £250,000, up from 16% when the tax was first introduced. This ‘fiscal drag’ means that around 95% of LBTT revenue comes from house sales over £250,000 and 22% from transactions over £750,000, which only accounts for around 1% of sales.

2. Steady rise in the count of receipts in 2024/25

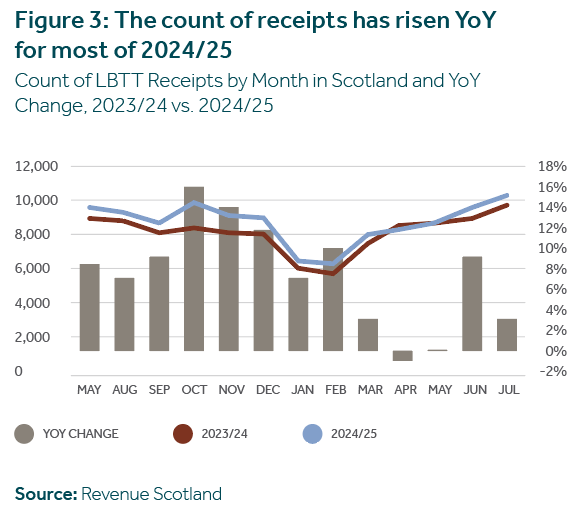

The count of LBTT receipts on a monthly basis has generally increased over 2024/25, with the rise compared to 2023/24 levels particularly noticeable in Oct-Dec 2024.

Receipt counts slightly dropped back in April 2025 and stabilised in May before year-onyear rises started again in Summer 2025, although at reduced levels compared with the late 2024 period.

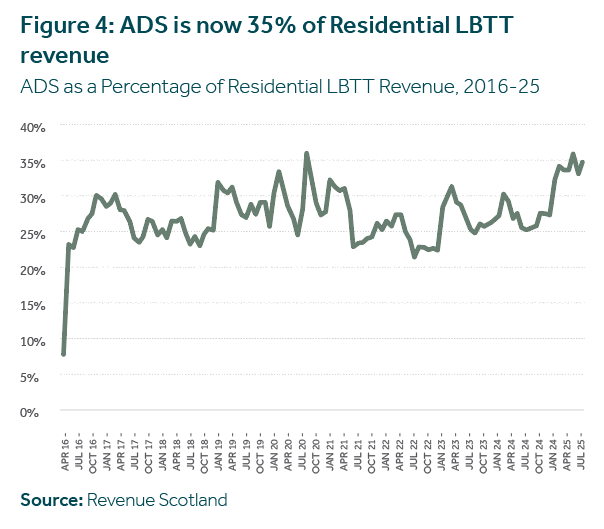

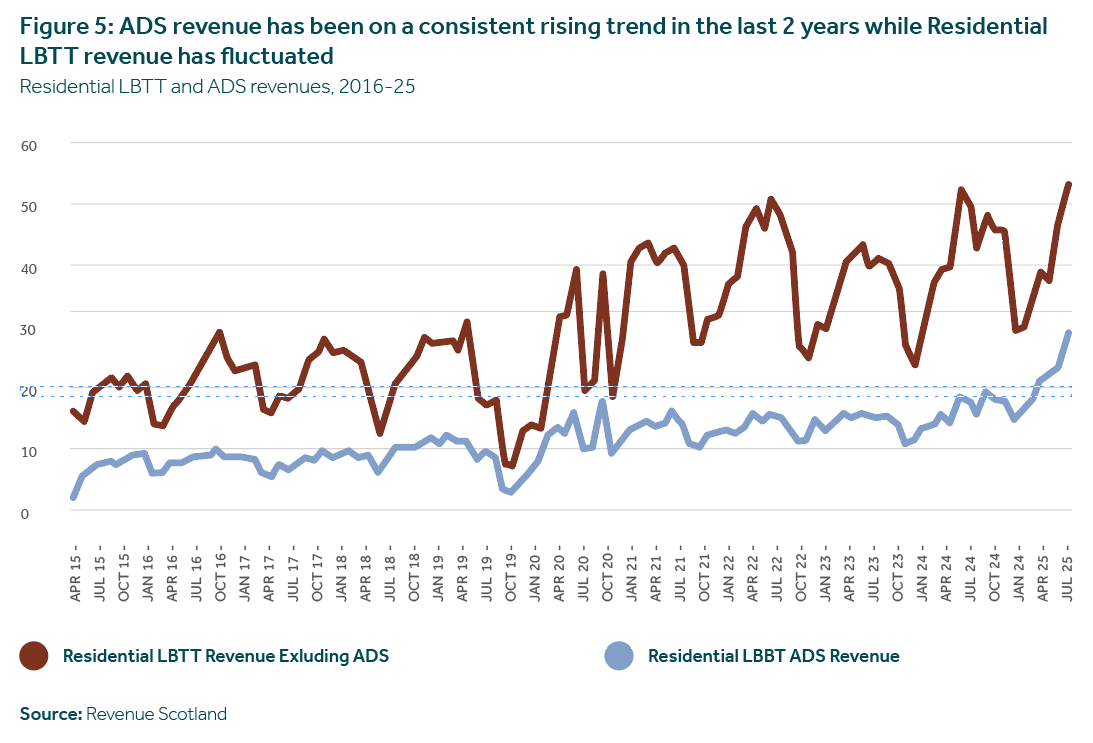

3. ADS revenue is climbing

Residential LBTT revenue has fluctuated in recent years due to housing market volatility. However, ADS has been on a steadier rising trend since 2022.

It was raised from 4% to 6% of the purchase price for second home transactions taking place after 16th December 2022 and then to 8% for transactions after 5th December 2024.

These rises in the tax rate have been a major reason for the climb in ADS revenues, which were around 25% of total Residential LBTT revenue in mid-2024 but are around 35% of such revenue in July 2025.

4. Geography lessons

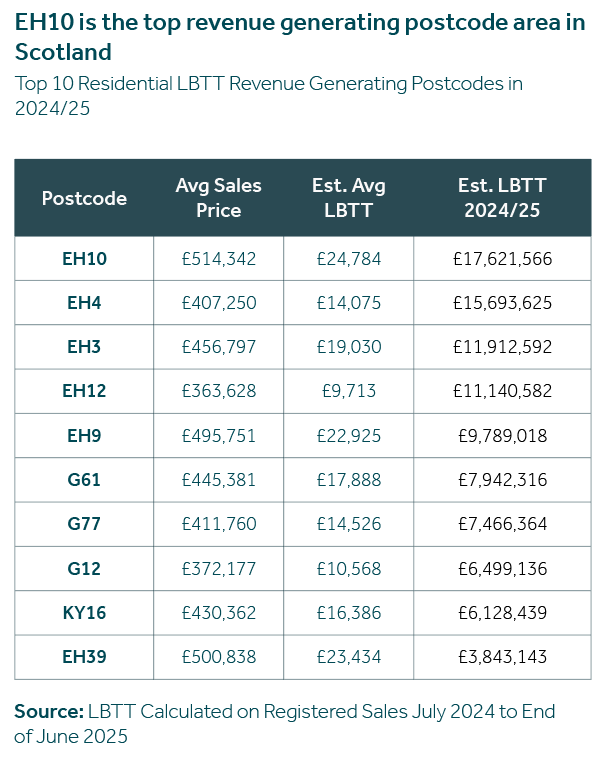

Analysis of Residential LBTT revenue by geography highlights some interesting trends across the country. In 2024/25, five of the Top 10 LBTT revenue generating postcodes were in Edinburgh, with three in Glasgow. KY16, which includes St Andrews, and EH39, which includes North Berwick, are the only postcode districts outside of the two major cities within the Top 10.

Total Residential LBTT revenue from the Capital is estimated to be just under £98 million in 2024/25 compared to the next highest area, Glasgow, which generated around £55 million.

The postcodes that generated the most revenue in 2024/25 were EH10 (including Morningside), EH4 (including Barnton and Cramond), EH3 (including the Edinburgh New Town), EH12 (including Murrayfield) and G61 (including Bearsden).

The highest average LBTT bill by area was in Fife in KY9 (including Elie) at just under £27,000, followed by EH10 in south-west Edinburgh at around £25,000, and by EH39 (including North Berwick) at £24,000.