Key findings explored

An adjusting sales market

Prices levelling off

The average house price in Scotland has been levelling off since September 2022, with growth slowing or stopping and some markets turning negative. Causes include the rising cost of mortgages, weakened buyer confidence, and a market correction after a period of strong house price growth. While this moderation in the market was anticipated before the mini-budget, the sharp rise in the cost of borrowing has accelerated it.

Activity falling

The number of registered sales at the start of 2023 is down around -10% across Scotland compared to the same period in 2022, with Glasgow down slightly less at -8% and Edinburgh contracting slightly more (-14%) from the relatively buoyant 2021-22 market conditions. This has seen market activity in both cities drop to the pre-pandemic levels of 2018 and 2019.

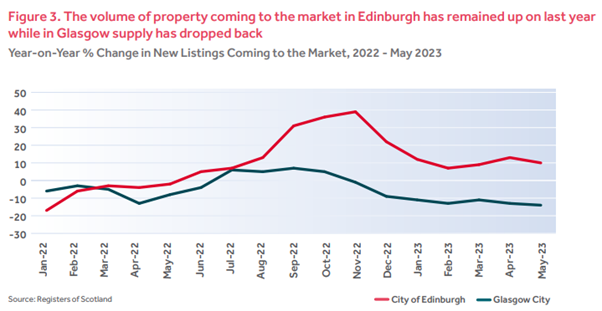

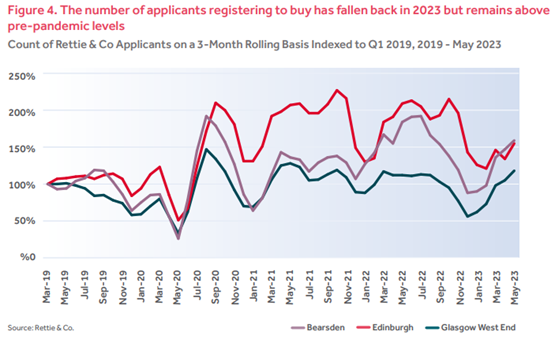

Supply and demand

Although sales have slowed, the value of properties being listed is broadly comparable with last year, although sales will take longer in the slowing market.

In terms of market demand, Edinburgh has had a notable contraction in the registration of new buyers in 2023. In Glasgow there is a more nuanced picture, with buyer registrations remaining robust in Glasgow West End, while in prime family neighbourhoods, such as Bearsden, they’ve retreated slightly from 2022 levels.

Looking ahead

Differences and nuances in the market between locations, price brackets and property types make navigating the current market more challenging. Equity rich buyers, less affected by mortgage rates, will likely continue to make purchases and there remains strong demand in prime markets. However, the market will be considerably less buoyant for first time buyers due to mortgage availability and affordability.

Mortgage challenges

Mortgage costs continue to rise

The main challenge for many is the rising cost of mortgages, particularly at a time of rising inflation and a cost-of-living crisis. The latest Bank of England decision to raise base rates to 5% to try to tame inflation will see mortgage rates rise further.

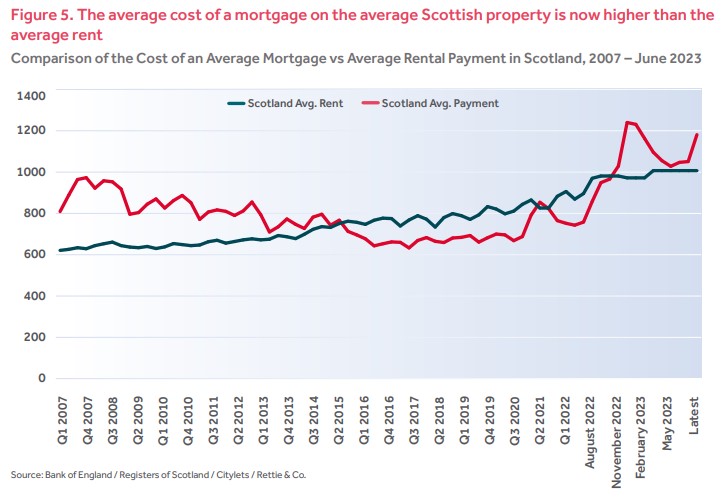

Mortgage v Rental costs

While the average monthly cost of a mortgage in Scotland was largely lower than the average rent over the 2015-21 period, this reverted in mid-2022 due to rising mortgage rates, putting pressure on affordability.

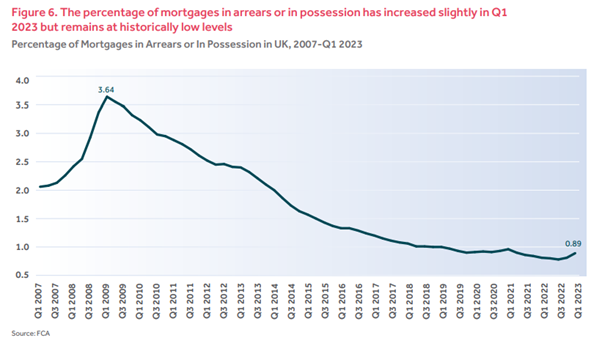

Still headroom in the market

The good news is that other fundamentals in the market remain less alarming. While the percentage of mortgages in arrears or in possession has risen slightly, this remains at historically low levels. While there will likely be an increase in arrears and repossessions if mortgage rates remain high or climb further as mortgage deals come to an end, there does seem to be some headroom in the market to cope with the upsurge in costs and a willingness by the banks to engage with customers to help them refinance.

New build difficulties

Multiple challenges

As we enter a period of slower or negative house price growth while material and labour costs remain high, the viability of new build sites will come under further pressure, slowing down housing delivery across tenures and affecting Scotland’s ability to respond to its housing availability crisis.

At the same time, significant changes to the planning system have seen many house builders concerned about the related uncertainty and confusion, potentially leading to sites being held up and not delivered until issues can be resolved.

New build activity could be subdued for some time to come, even with a wider market recovery.

Rental market crisis

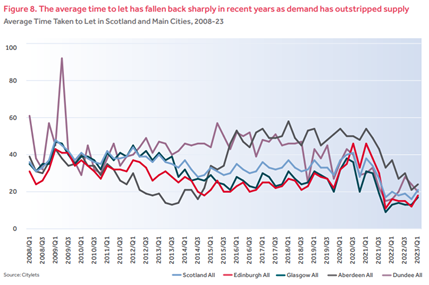

Affordability and time to let

The housing shortage is clearly impacting affordability in the rental sector. Over the past five years, rents in Scotland and Edinburgh have seen an annual compound growth rate of over 5%, while, in Glasgow, recent rent increases have pushed this to over 8%.

At the same time, the drop in rental supply is driving down the average time taken to let a property. Having historically been somewhere between 20-30 days, this figure has fallen to 10-15 days in the main cities.

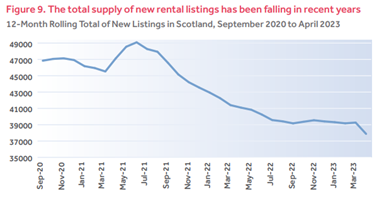

New listings fall by more than a fifth

While there were around 49,000 rental listings in Scotland in the 12 months to Summer 2021, in the past 12 months the figure has fallen to under 38,000, which is a reduction of more than 20%. Source: Rightmove

Impact of legislation

Over the past six years, the Scottish rental market has seen numerous interventions that have changed how the sector operates, including, most recently, the rent freeze/cap and evictions ban. These interventions have made the financial incentives to operate in the Scottish PRS, at best, more challenging. With further new legislation in the pipeline, there is likely to be a further reduction in supply at a time of increasing demand, as more landlords choose to leave the sector.

A Subdued Outlook

As we highlighted in our Winter Briefing at the end of last year, we anticipate that average house prices will fall back over the course of 2023 by around 5% on the central forecast and may see continued weakness in 2024 before returning to positive growth in 2025.

Figure 10. Average house prices are forecast to fall back by around 5% in 2023 based on our central forecast

Scottish House Prices (Actual and Forecast), 2023-2026. Source: Registers of Scotland/Rettie

Although the outlook has arguably worsened since our previous briefing, we are not anticipating the 15-20% fall that has been forecast by some commentators. This is because unemployment and arrears remain at low levels and banks are still lending, although at reduced volumes and higher rates. However, our prognosis could become gloomier over the course of 2023-24 if interest rates continue to rise (as a result of high inflation) and mortgage rates follow.

We believe that transactions will drop back 15% over the course of the year, but the downside scenario of a 25% reduction has become more likely with the recent 0.5 percentage point rise in the base rate.

As always, different markets will be impacted differently. While we expect prime markets to remain more robust, there can be no doubt that first time buyers and leveraged investors will find market conditions more challenging. These pressures will weigh down on all tenures, limiting people’s choice and housing options. In this context, current legislative reform is not helping.