Prices relatively robust, activity down

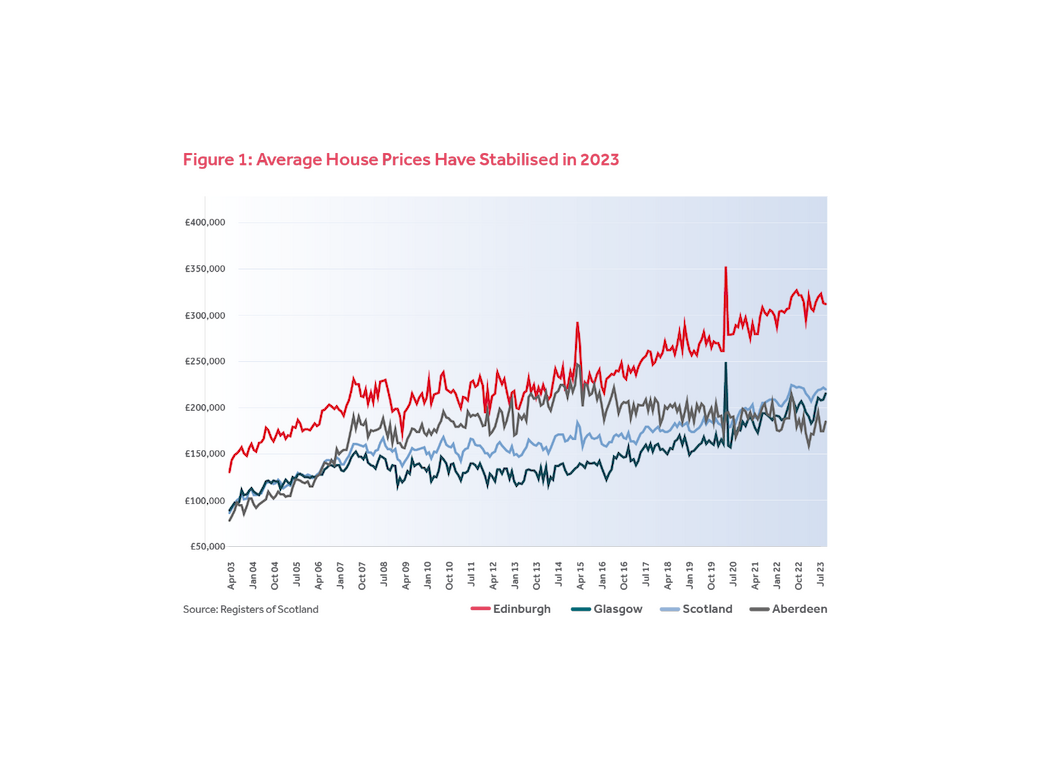

Despite the increase in the cost of new mortgages, average house prices have remained relatively robust in the past year, supported by tighter supply. Latest figures for October 2023 show the average Scottish house price down 1.5% on the same month last year. However, the average house price over Jan-Oct 2023 remains 1% up when compared to the first 10 months of 2022.

The new build market has been more severely impacted, with sales down 15% in the first 10 months of 2023. As well as the reduction in demand, the new build sector has also faced supply-side problems with rising construction costs and labour market and supply chain pressures. All of this has impacted on the viability of development in many areas, slowing delivery.

Although transactions have fallen, we seem to be gradually moving back to pre-pandemic patterns despite the economic upheaval of the last year or so.

There are some positive signs emerging around future sales expectations, consumer confidence and mortgage lending, which point towards stabilising and improving market conditions as we enter 2024. However, the challenges of above target inflation, relatively high interest rates and a cost-of-living crisis remain for many.

Mortgage costs dampen affordability

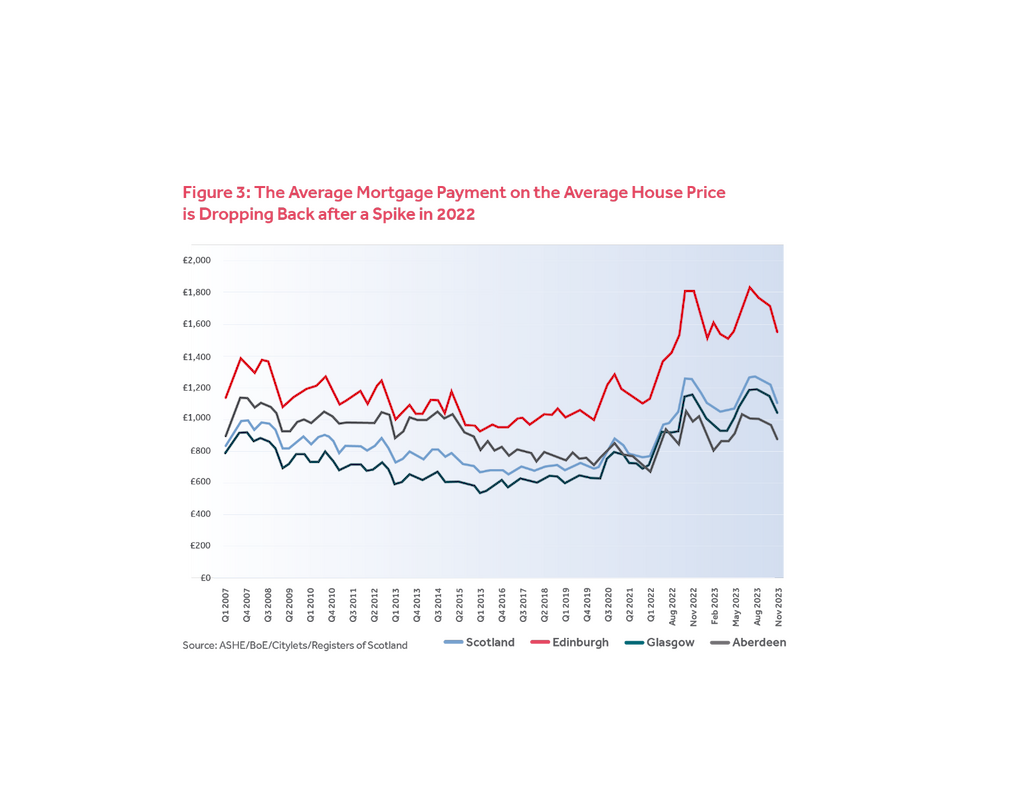

The sharp increase in mortgage rates has had a dampening effect on the housing market over the past year. This can be seen clearly when tracking the cost of the average mortgage payment. In 2020, the average mortgage payment in Edinburgh was under £1,000pcm, before peaking at £1,800pcm in mid-2023. With mortgage rates reducing, this figure has pulled back to nearer to £1,500pcm. If rates stabilise, or continue to fall, this will improve affordability and confidence in the market.

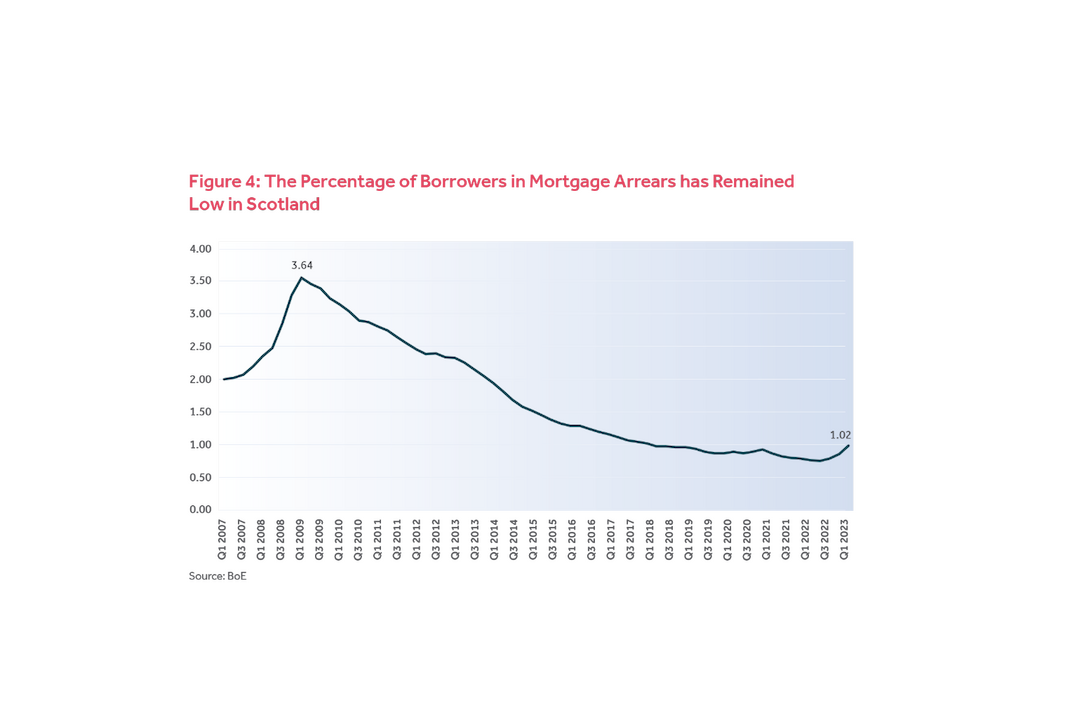

While there has been a small upturn in mortgage arrears, the steps lenders are taking to mitigate rate shocks seem to be working, with the arrears well below the level seen at the time of the Global Financial Crisis in 2008/09. This has reduced the potential impact of distressed sales (sales where owners are forced to sell due to financial difficulty).

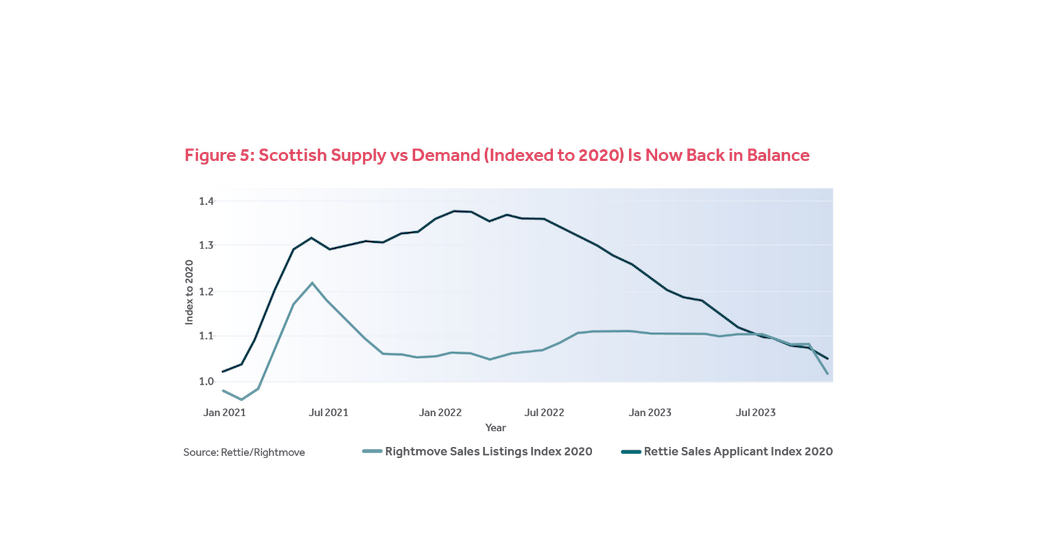

Signs of a stabilising market

Analysis of supply and demand indices in the market over the past few years shows that demand levels are now returning to pre-pandemic levels and are in line with supply pre-pandemic levels, which has led to a stabilisation in prices.

In Edinburgh, unlike the wider Scottish market, supply increased from mid-2022 onwards. This has been driven by sellers looking to take advantage of strong sales values, as well as a proportion of landlord investors electing to exit the sector due to increasing costs and regulations while sales values are high.

By contrast, Glasgow has had a more consistent pattern, with less fluctuations in both supply and buyer demand. However, these trends do vary within cities depending on location and property type.

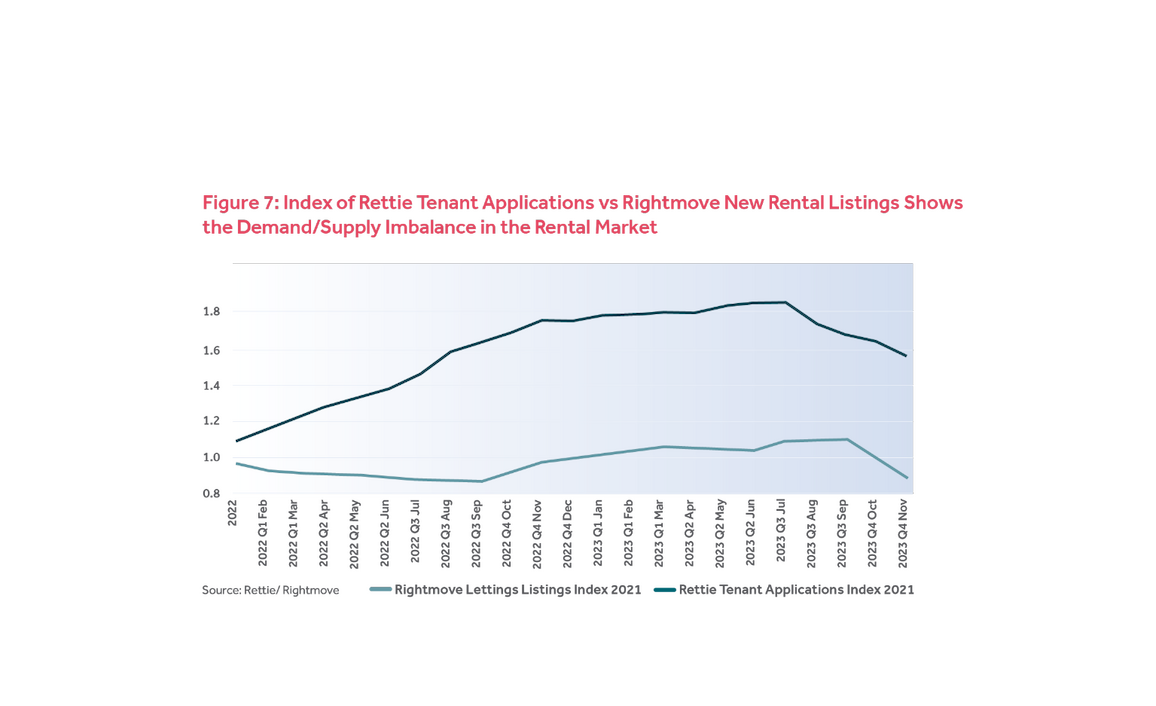

Rental market sees excess demand

The average rent of newly listed properties across Scotland has increased sharply in the past year.

As of Q3 2023, Citylets is reporting the average advertised rent in Scotland at £1,115pcm, with rents of £1,208pcm in Glasgow and £1,546pcm in Edinburgh - annual increases of 14%, 16% and 17% respectively.

This pressure on the rental sector is largely due to a demand/supply imbalance. Analysis of new listings coming to the market shows that, over the past couple of years, new supply has contracted by around 7%, while demand within the market has continued to rise. The number of tenant applications received by Rettie is at around 1.6 times 2021 levels, down from a peak of 1.8 earlier this year. By contrast, new listings are currently at 0.9 of 2021 levels.

The current imbalance is reflected not only in rising rents but also in the time it takes to let a property (TTL). Having historically averaged between 30 to 40 days, the average TTL in Scotland is now down to 18 days, with TTL in the major cities even lower.

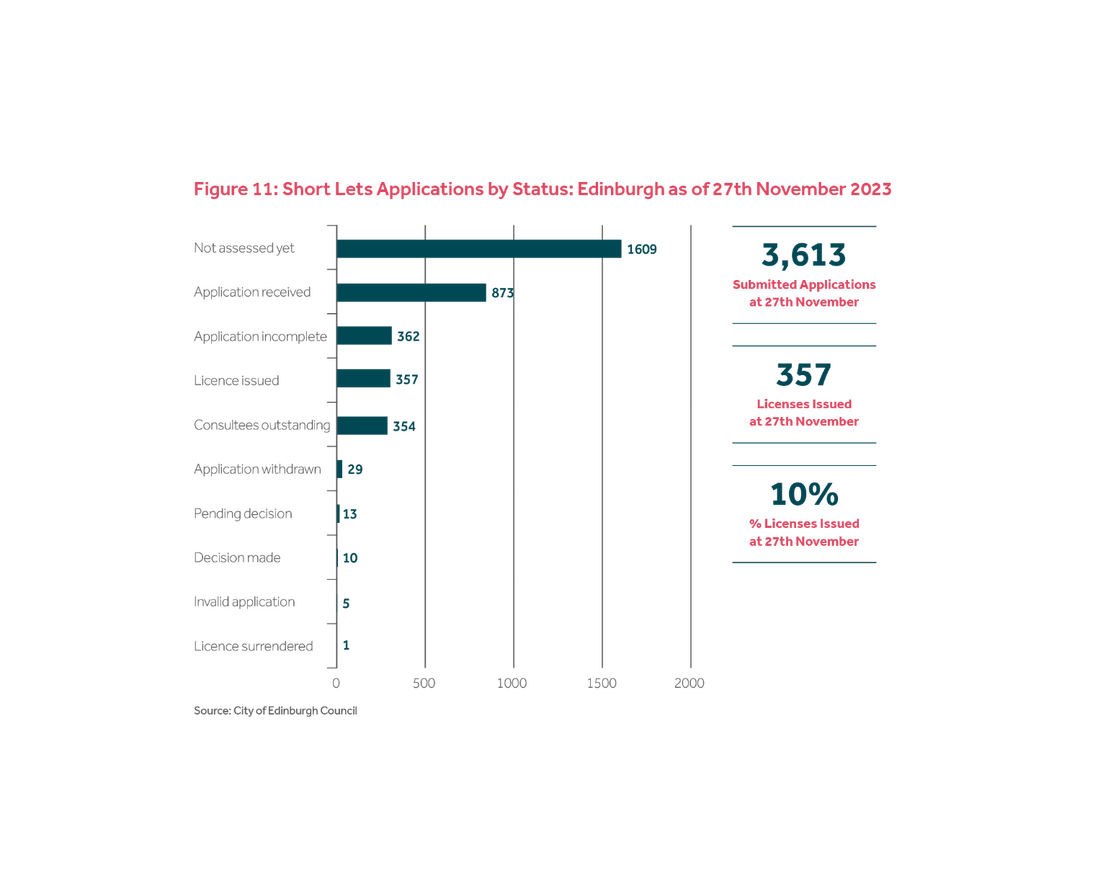

Short term lets

In Scotland, licensing is now mandatory for all short-term lets (STLs). Local authorities can designate ‘short-term let control areas’ to manage high concentrations of STLs and, within control areas, such as Edinburgh, use of a dwelling house, which is not a host’s principal home, as an STL will require planning permission.

However, Scotland’s Court of Session recently ruled that some aspects of Edinburgh’s policy were unlawful. While Edinburgh Council said it would make changes to comply with the court ruling, the Court has again ruled again against the Council, with the judge calling the application process unfair and illogical in terms of potential outcomes.

As of 27th November 2023, there had been 3,613 license applications submitted to the City of Edinburgh Council, of which only 357 licenses have been issued. Although many of these applications have still to be considered, there is considerable uncertainty about the future for the sector in the city and in other Scottish tourist areas, particularly given recent rulings.

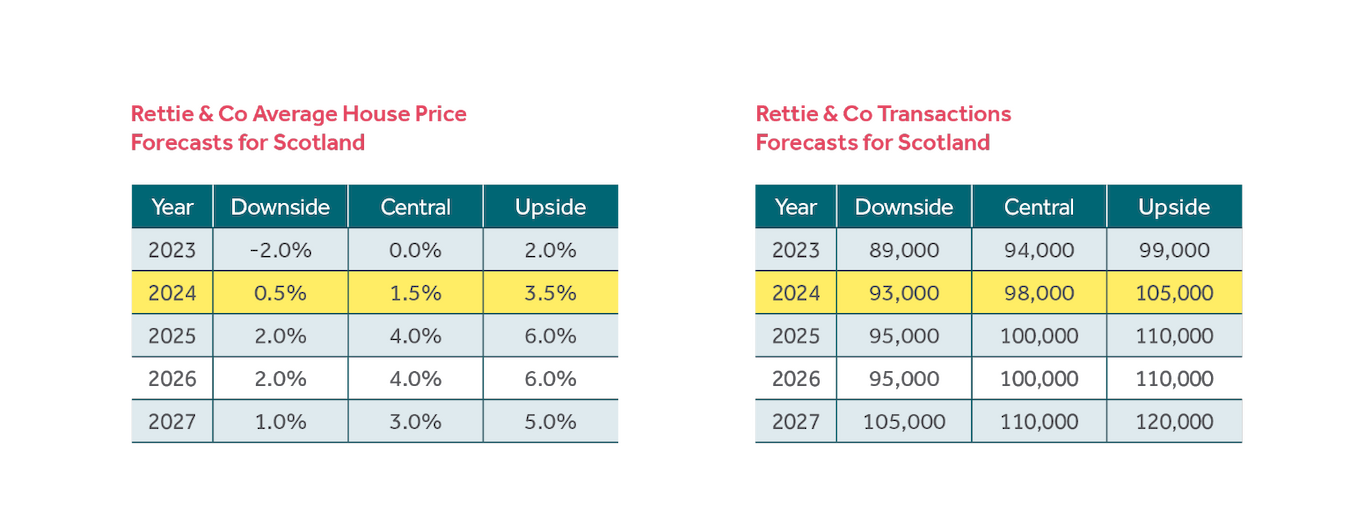

Our Rettie forecast

While mortgage rates have been coming down, they will remain above historic levels for a time, exerting continued downward pressure on the overall average price across Scotland. In saying this, properties are still coming to market and there remains active demand, although not at the levels seen over 2021 to mid-2022.

In our central forecast, we expect average prices to rise fractionally next year, by around 1.5%, before moving back closer to the long-term trend (of around 4%) in subsequent years if the economy recovers as anticipated. It will take time for the whole market to adjust to higher interest rates, as people gradually come off fixed term deals, which will probably lead to average house price growth at reduced levels for a time.

We also anticipate that sales activity will stabilise and start to recover. Transactions look like being around 94,000 for 2023 and we believe that they will be maintaining around the 100,000 level for the next few years. For buyers and sellers alike, this stabilisation in market conditions will give some confidence to enter the market.

This will vary across geographies and property types.

In terms of the rental market, with the cost of the average mortgage currently more than the average advertised rent, there is likely to be continued pressure on the private rented sector (PRS) as demand has not dampened in the way it has in the sales market.