The Covid Effect

An Unprecedented Event

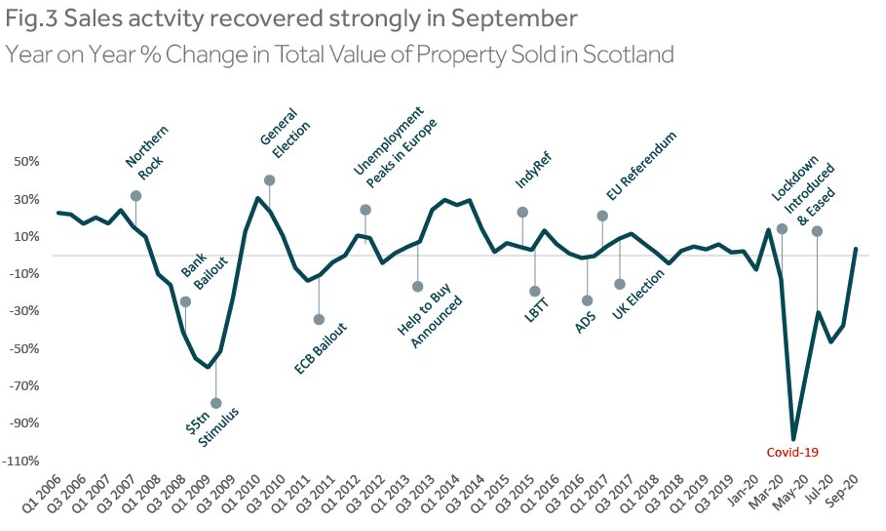

The Covid-19 pandemic and subsequent lockdown has created a market intervention unlike any experienced before, with transactions being constrained by state intervention on health grounds rather than economic conditions driving consumer choices, as was the case during the Global Financial Crisis (GFC). While we are still navigating the pandemic and its potential economic and social consequences, so far, the Scottish property market has experienced a markedly different pattern of activity compared to previous market downturns.

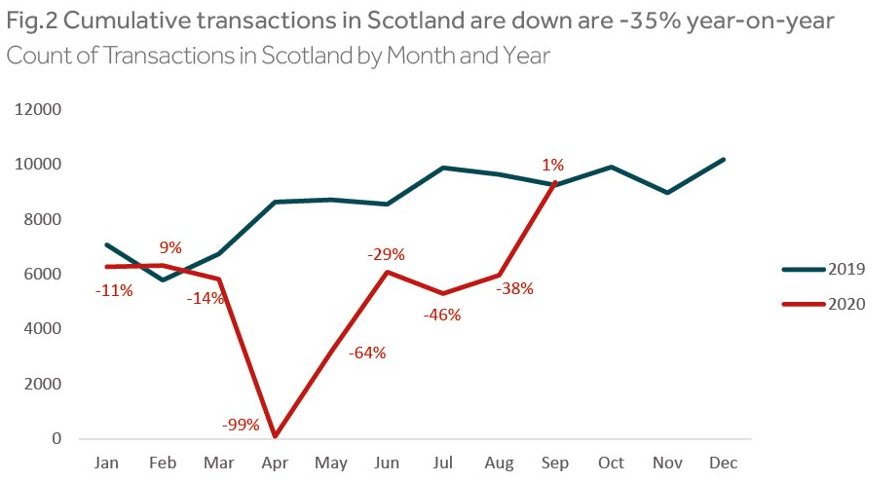

The first thing to note has been the sharp fall and then recovery in activity. Over the course of 2018 and 2019, the Scottish market had seen a plateauing of transaction growth after a period of strong growth and this trend had continued into the start of 2020. With the effective closure of the market under the lockdown restrictions, transactions almost ceased completely, with just over 100 registered sales in April across Scotland when there would typically be over 8,000. This fall was more precipitous than during the GFC but the recovery was almost immediate after lockdown lifted at the end of June. New properties coming to the market surged in the wake of lockdown, with the pent-up activity from the Spring market displaced into the Summer months. Property listings in the weeks after lockdown in Edinburgh and Glasgow surged 50% to 100% higher than the same time in 2019. This supply meant that by September registered sales activity was at parity with September 2019, although the cumulative number of registered sales to Q3 remained -35% down. However, due to the lag between sales being agreed and registered, the true level of the market recovery will likely not be seen until the full year figures for 2020 are published.

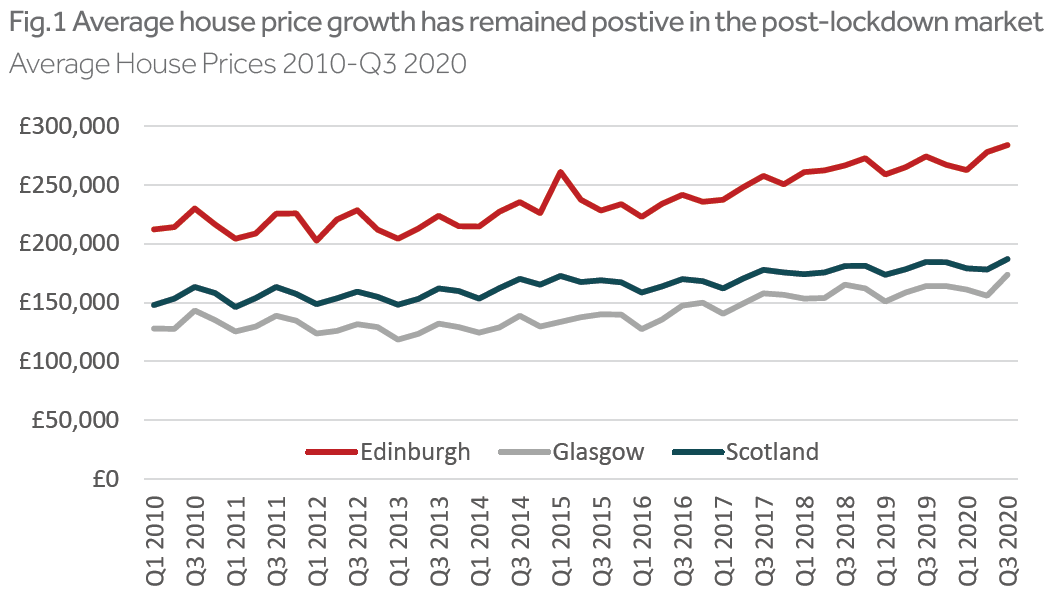

One similarity between current market conditions and previous downturns has been the robustness of house prices. Much like during the GFC, house prices in the wake of the lockdown have not experienced significant downward movement and have even seen growth in some localised markets. Pent-up demand, combined with people reconsidering their life aspirations has supported sales values.

Looking ahead, there remains much uncertainty as the furlough scheme comes to an end and Brexit moves back into the headlines. This said, the pandemic has made many households reconsider the importance of a home as more than just a dormitory and this is underpinning demand and movement in the market, as well as shaping the character and location of property being sought.

Forecasts

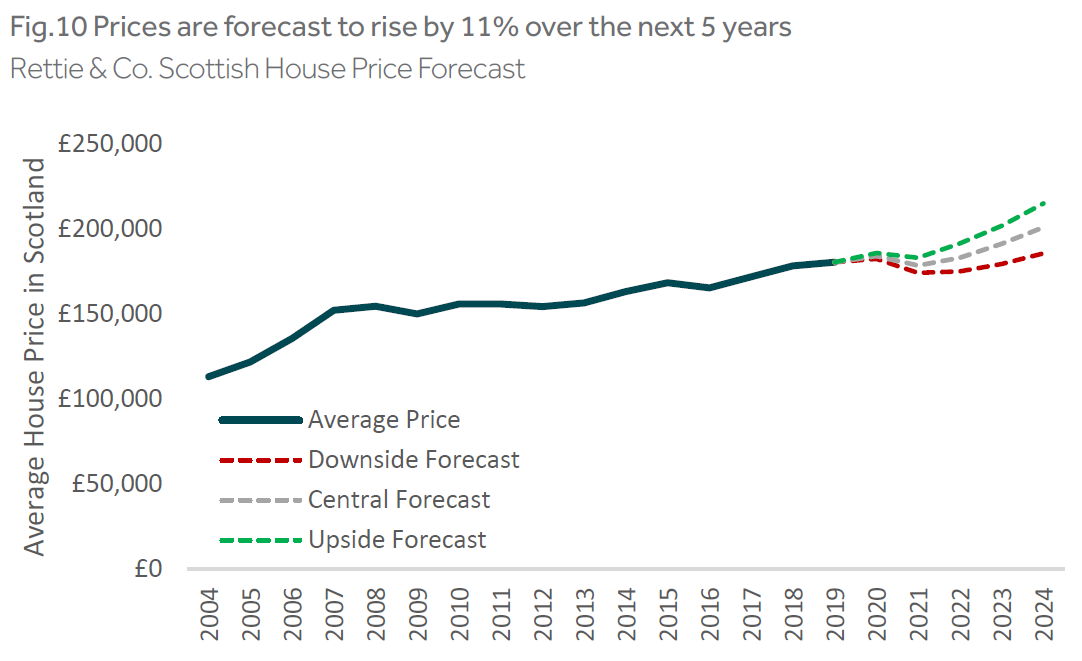

We have revised our forecasts since the lockdown phase, but not by much. We were correct in anticipating that there would not be the house price crash that some commentators were suggesting. Instead, house prices have risen this year to date, despite the collapse in the economy, as the surge in demand post-lockdown has met a surge in supply of properties coming onto the market. As the market moved into Autumn, this demand appears to have been largely sated in most locations and the market in some areas is now looking at over supply.

This will likely push back prices into next year, when coupled with stronger economic headwinds as a result of the ending of generous government support packages, will likely dampen sentiment further. However, the correction in house prices will probably be limited, as they were in 2008/09, unless there is a flood of distressed sales. With very low interest rates and the banks not as over-stretched as they were in the previous recession, we are not anticipating a high level of distressed sales, unless, for example. there is a marked and sustained increase in unemployment or a collapse in lending.