Prices Dampening, Activity Falling

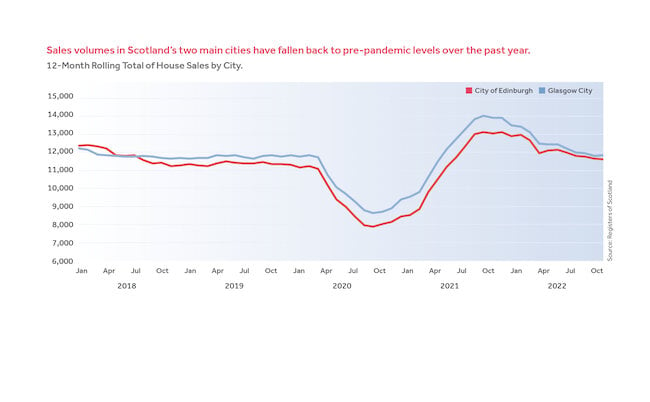

It seems clear that there is a wider market dampening effect on house prices caused by rises in interest rates and inflation, although this is only mild for now. In terms of market activity, sales in 2022 have fallen back compared to the high levels of activity experienced in 2021. This is not unexpected, as 2021 represented an unusual market, driven by pent-up pandemic related demand.

In the year to October, sales in Edinburgh were 11% lower than the same period last year, while Glasgow reported a 15% fall. It’s worth noting that while activity in the past year is down on 2021 levels, sales activity across Scotland remains 3.2% up on pre-pandemic 2019 levels.

While there are undoubtedly many challenges facing the market, it’s important to highlight that, when accounting for inflation, the recent increase in property prices is less acute than previous housing bubbles. For this reason, it’s not anticipated that the market will see similar price corrections as previous cycles.

Demand Still Running Ahead of Supply

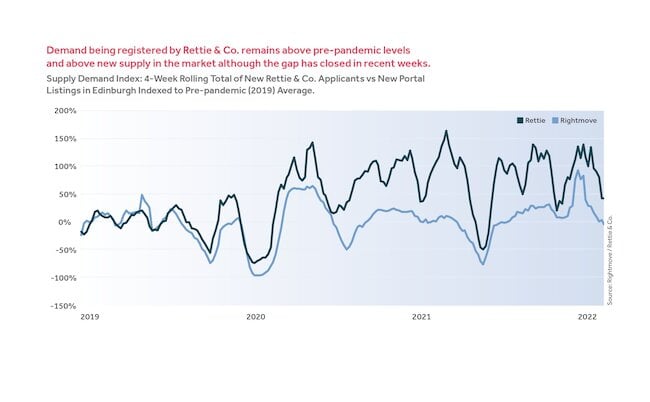

Over the last three years, Rettie have consistently registered a higher level of buyer demand than supply coming to the market. As the latest figures to November 2022 show, the gap between demand and new supply has narrowed. However, there are still more new applicants than new stock, which supports the modest level of price rises still being seen.

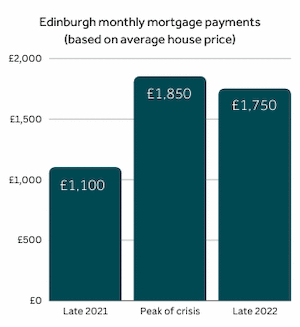

Rising Cost of Borrowing

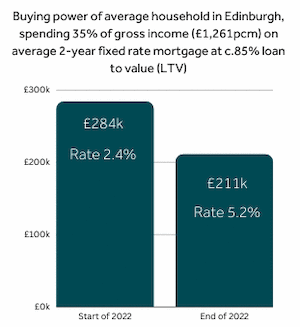

The combination of rising house prices and the recent spike in the cost of borrowing, means that the increase in the cost of borrowing has led to a fall in the buying power of the average household income by around a quarter.

This illustrates how the reach of many buyers, especially first-time buyers and younger households with less equity, will be impacted. As first-time buyers are often the most reliant on available lending and tend to lack the equity reserves of those already on the property ladder, this group is once again most likely to see a drop in market activity, which will have an impact on chains higher up the housing ladder.

However, it’s important to note that, when adjusting for inflation, mortgage costs have risen sharply, but they remain within historical precedence.

The New Build Market

Rettie has a market leading database tracking over 2,600 historic new build developments across Scotland. Using this resource, we’ve noted an upturn in discounts and incentives being offered to the market.

However, our own experience, in both the new build and wider markets, is that demand in Glasgow and Edinburgh remains high, especially in prime locations. This experience is borne out by the fact that premiums above Home Report are still being achieved by our sales teams, emphasising that not all homes are the same and knowledge of submarkets and geographies is crucial in understanding the changing market conditions.

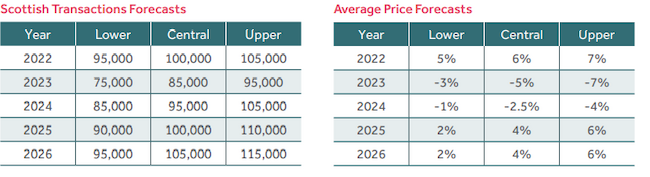

Our Rettie Forecast

Looking ahead, there can be no doubt that the housing market is set to have a challenging time over the next year and this will probably continue into 2024. We anticipate that, while there is likely to be a cooling in price, it will be transactional activity that will be most impacted as households weather the current uncertainty.

The market should pick-up again after 2024, when most of the fallout from events of this year should have washed through, but the world is an uncertain place just now and, as ever in forecasting, we assume ‘other things being equal.’

Our forecasts suggest (on a central basis), a fall of 15% in market activity (transactions) in 2023 before gradual recovery back to trend over the following two years.

Average prices look like topping 6% in 2022 based on data to October, but reversals now seem very likely for 2023 and 2024 with continued rises in interest rates and an economic recession. Again, we are assuming a gradual return to trend as the economy recovers.